If you trade the currency markets and have any sort of fundamental bent to analyzing the markets (which you absolutely should), then you may have heard about a country’s reserves (also known as FX reserves or foreign exchange reserves).

Reserves are important because they help to signify the amount of influence a country or jurisdiction has in controlling its exchange rate.They represent cash and other forms of reserve assets held by a central bank (or reserve bank or other monetary authority) in foreign currencies.

They help to balance payments of a country against the liabilities that it issues and helps encourage stability in its currency and financial markets.These commonly consist of cash, bank notes, bonds, deposits, and various government securities.The US dollar is the most commonly held reserve asset as the world’s top reserve currency.The euro, British pound, Japanese yen, and Chinese renminbi are also common as well.

When a country depletes its reserves, the confidence in the national currency can rapidly deteriorate.While this is more common in emerging and frontier markets, this does occasionally occur in developed markets as well.

Example: United Kingdom, 1992

The UK’s reserve situation in 1992 is perhaps the most famous example of how a currency can move in response to the situation involving its foreign reserves.

During the early part of the 1990s, the British pound had kept in line with the German mark.

The pegging system was put in place to enhance monetary and economic cooperation throughout the Euro area as a precursor to the Euro.

However, the Bank of England did not have sufficient reserves to maintain the Pound indefinitely within the European Exchange Rate Mechanism (ERM) – the predecessor to the European Monetary Union and the adoption of the Euro. The rate was maintained at 2.7 German Marks per Pound.

Until that point, the UK was forced to keep its interest rates artificially low due to the perceived benefits of greater monetary and economic cooperation between European countries. However, this was not a sustainable set of conditions. The UK needed higher interest rates to reduce its inflation rate from 8%, which created unnecessary price pressures and inefficiencies within the economy.

In order to keep the Pound pegged to the Mark, the Bank of England had to purchase its own currency with its foreign reserves to maintain the Pound within the desired range. Many market participants realized that the Bank of England could not indefinitely resist market forces with its economic situation and would eventually have to float the currency.

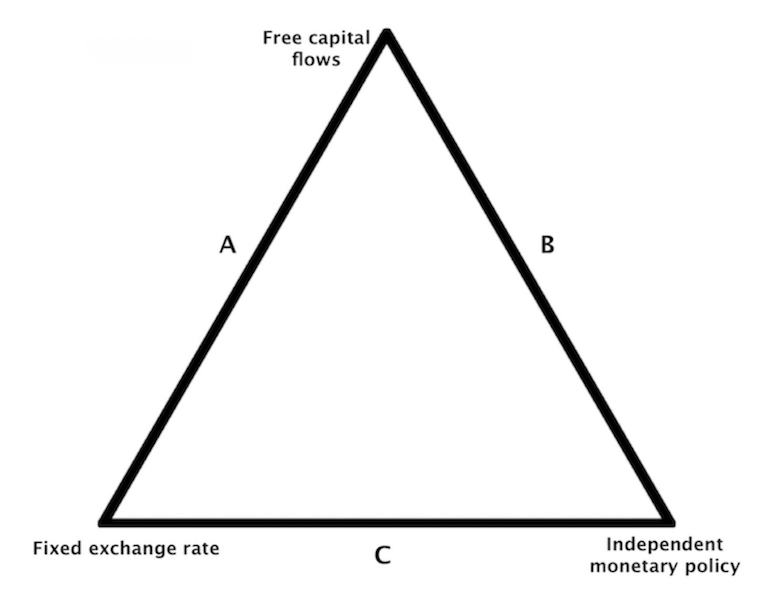

As explained in a different article on currency regimes, if a country wants a fixed exchange rate and an independent monetary policy at the same time, it must restrict the flow of capital (or such flows must be negligible to avoid breaking the currency peg).

If it wants to allow for the free flow of capital (which helps encourage foreign direct investment), then it must forgo having an independent monetary policy.

The Bank of England wanted to avoid having to restrict capital flows, which can be very difficult.

Therefore, the only option left was to surrender its ability to have an independent monetary policy.

Under these circumstances, inflation eventually spiraled out of control. It was speculated by traders that the BoE would need to remove the pound from the ERM to address the situation. As a result, they opted to short the currency.

The BoE responded to speculative pressure by increasing interest rates to attract inflows into the pound instead of using its own reserves. Interest rates were raised from 10% to 12%, and then to 15%. This made the currency more expensive to borrow and more attractive to lend.

However, the market wasn’t convinced and knew that an interest rate defense wouldn’t be effective, and that the BoE would eventually exhaust its reserves entirely.

After two years of joining, the British government finally yielded and allowed the pound to fall out of the ERM. The pound subsequently fell by around 15% against the German mark in the following few weeks. This provided traders who had shorted the pound with a remarkable windfall. The losses for the UK Treasury, and consequently UK taxpayers, amounted to over £3 billion.

Foreign Exchange Reserves: How They’re Acquired

Why do countries have varying foreign exchange reserves, and how do they acquire them?

Foreign exchange reserves are accumulated in the same way that an individual accumulates savings – by earning more than they spend. This can be achieved by exporting more than importing, which maintains a positive trade balance.

This can be raw materials (oil, gold, coal, etc.), or secondary goods (e.g., importing lumber and exporting wooden furniture).

Or by selling more services to the rest of the world than it takes in – e.g., tourism, attracting foreign businesses, receipt of foreign aid, remittances from workers abroad.

They can also increase reserves by borrowing from the rest of the world through loans or by issuing their debt to foreigners.

If a country lacks resources to export, then it must build reserves through productivity. They can do this by selling services or importing materials to create value additive products to export back out.

Exporters and other companies that earn foreign currency can exchange that for domestic currency with a commercial bank (which is under the purview of the central bank) or directly with the central bank itself.

For instance, when Chinese exporters trade with the US, the exporters will exchange their goods for US dollars. Then they exchange those dollars at a state bank (or PBOC directly) and get renminbi (also known as yuan or CNY). The central bank increases the amount of currency in circulation based on whatever the market demand for it is.

The exporter would then take the domestic currency it received from the central bank, and the central bank would acquire their USD it received in the cross-border transaction.

China’s central bank also formerly used to assist exporters, at least in a more material way, by keeping a peg with the USD to keep its currency artificially low.

This helped increase demand for exported products and thus China more easily acquired reserves that way.

The PBOC would typically take those dollars and invest them into US Treasuries (a form of dollar reserves) in order to get the extra yield rather than just getting the spot rate.Moreover, US Treasuries are assumed to not have any credit risk.

If China were to sell goods and services to Germany, for example, it would receive euros.The central bank could, if it wanted to, take those euros and convert them to dollars.It can also take dollars and convert them to other foreign currencies or its own domestic currency.Currency reserves are often used to manage exchange rate fluctuations.

If the CNY is depreciating and the PBOC wants to control that to support its domestic policy objectives it can sell foreign reserves in exchange for its own currency.

Central banks typically like to keep their reserve accounts steady.So, if they don’t wish to allocate any more to US dollars, for example, they probably won’t be a big buyer of US Treasuries if their accounts are already “topped off” with USD.This can be informative in figuring out where Treasuries are likely to go price-wise.

So, reserve growth is a function of the balance of payments, which influences the supply and demand for different currencies.

At the most fundamental level, when you buy a currency, that’s basically a claim on the future wealth of a country.

Or the future wealth of one country relative to another if you’re borrowing in another currency to fund the purchase of the other.

The total growth in foreign exchange reserves is a function of the growth in productivity and growth in the labor force, though the demand for any given currency will be dependent on the specific conditions and factors that affect its relative attractiveness.

The US dollar will decline over the long-run.Foreign accounts are already quite saturated with dollar-denominated assets and the US spends more than it earns, and its balance sheet is deteriorating with a balance of payments and government deficits.

However, over the short-run, a myriad of factors have been going in the US dollar’s favor – e.g., high nominal and real interest rates relative to the rest of the world, re-buildup of the Treasury’s general cash account (which diminishes bank reserves), and heightened demand for its foreign repo pool.

The US, in its unique (and vulnerable) position as having the world’s top reserve currency

The United States does not have large reserves, but what it does have is the power to print the world’s reserve currency.

The ability to print “the world’s money” and have it accepted by the rest of the world is the most valuable economic power a country can have.

It’s an ability that only a major world reserve currency country (especially the US) has with respect to the overall privilege it creates due to the enormous borrowing and spending benefits and also the ability to alter geopolitical incentives through the use of sanctions.

It is right up there with having the world’s top military power.

But at the same time, a country that does not have sizable foreign exchange reserves, which is the position the US is in, makes it susceptible to not having enough “world money”.

This means that the US is very powerful right now because it can print the world’s money but, on the same token, it would be very vulnerable if it lost its reserve currency status.

The Importance of Foreign Exchange Reserves and the US Dollar

Or the future wealth of one country relative to another if you’re borrowing in another currency to fund the purchase of the other.

The total growth in foreign exchange reserves is a function of the growth in productivity and growth in the labor force, though the demand for any given currency will be dependent on the specific conditions and factors that affect its relative attractiveness.

The US dollar will decline over the long-run.Foreign accounts are already quite saturated with dollar-denominated assets and the US spends more than it earns, and its balance sheet is deteriorating with a balance of payments and government deficits.

However, over the short-run, a myriad of factors have been going in the US dollar’s favor – e.g., high nominal and real interest rates relative to the rest of the world, re-buildup of the Treasury’s general cash account (which diminishes bank reserves), and heightened demand for its foreign repo pool.

The US, in its unique (and vulnerable) position as having the world’s top reserve currency

The United States does not have large reserves, but what it does have is the power to print the world’s reserve currency.

The ability to print “the world’s money” and have it accepted by the rest of the world is the most valuable economic power a country can have.

It’s an ability that only a major world reserve currency country (especially the US) has with respect to the overall privilege it creates due to the enormous borrowing and spending benefits and also the ability to alter geopolitical incentives through the use of sanctions.

It is right up there with having the world’s top military power.

But at the same time, a country that does not have sizable foreign exchange reserves, which is the position the US is in, makes it susceptible to not having enough “world money”.

This means that the US is very powerful right now because it can print the world’s money but, on the same token, it would be very vulnerable if it lost its reserve currency status.